OFFICE HOURS

M-

Sat: 9:00 AM to 8:00 PM

Call 724-

106 Apollo Road, Suite 2

Mount Pleasant, PA 15666

© 2001 -

Schedule Your Taxes

724-

2019 Tax Changes

Due Date of Return

The due date for filing a 2019 return is Wednesday, April 15, 2020 for most filers.

Standard Deduction

The standard deduction for taxpayers who do not itemize deductions on Form 1040, Schedule A, has increased. The standard deduction amounts for 2019 are:

Married Filing Jointly or Qualifying Widow(er) – $24,400 (increase of $400)

Head of Household – $18,350 (increase of $350)

Single or Married Filing Separately – $12,200 (increase of $200)

Taxpayers who are 65 and Older or are Blind

For 2019, the additional standard deduction amounts for taxpayers who are 65 and older or blind are:

Single or Head of Household – $1,650 (increase of $50)

Married taxpayers or Qualifying Widow(er) – $1,300 (no change)

Personal Exemptions

The deduction for all personal exemptions is suspended (reduced to zero), effective for tax years 2018 through 2025.

For 2019, the gross income limitation for a qualifying relative is $4,200.

Alimony

For any divorce or separate maintenance instrument executed after December 31, 2018, (or executed on or before December 31, 2018 and modified after that date if the modification expressly provides that the amendments made by the Tax Cuts and Jobs Act, Section 11051, apply to such modification), alimony and separate maintenance payments are no longer deductible by the payor spouse. Additionally, alimony and separate maintenance payments are no longer included in income by the recipient of the payments.

The 2020 Form W-

Has been redesigned and no longer uses the concept of withholding allowances. It replaces complicated worksheets with more straightforward questions that make accurate withholding easier for employees. Employees who have submitted Form W-

Entry spaces on 2019 tax forms are shown for dollar amounts only (no cents).

Schedule C-

Form 8965, Health Coverage Exemptions, and its instructions have also been made obsolete for 2019.

Form 1040-

As required by the Bipartisan Budget Act of 2018, Form 1040-

Eligible Long-

For 2019, the maximum amount of qualified long-

$420 – age 40 or under

$790 – age 41 to 50

$1,580 – age 51 to 60

$4,220 – age 61 to 70

$5,270 – age 71 and over

Health Savings Accounts

Health Savings Account (HSA) Deduction

For 2019, the annual contribution limits on deductions for HSAs for individuals with self-

Standard Mileage

For 2019, the following rates are in effect:

58 cents per mile for business miles driven

20 cents per mile driven for medical or moving purposes

14 cents per mile driven in service of charitable organizations (no change)

The standard mileage rate for business cannot be used to claim an itemized deduction for unreimbursed employee travel expenses during the suspension of miscellaneous itemized deductions that are subject to the 2% of AGI floor.

The moving expense deduction is not allowed through 2025 and the exclusion from income of moving expense reimbursements from an employer is also suspended. The only exception is for active military service members who move pursuant to a military order to a new permanent duty station.

Deduction for Qualified Business Income

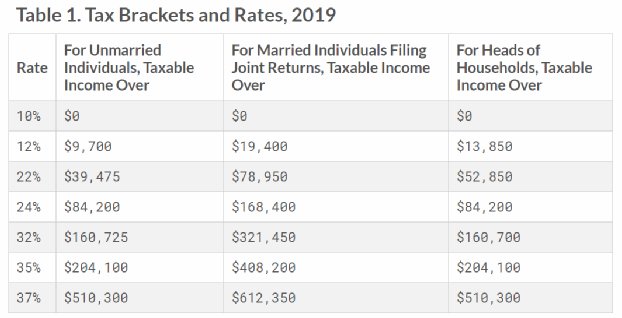

For 2019, the threshold amount is $321,400 for Married Filing Jointly returns, $160,725 for Married Filing Separately returns, and $160,700 for Single and Head of Household returns.

Retirement Savings Contribution Credit

In order to claim this credit, the taxpayer’s modified adjusted gross income (MAGI) must not be more than $32,000 for Single, Married Filing Separately, or Qualifying Widower (increase of $500). MAGI must not be more than $48,000 (increase of $750) for Head of Household, and $64,000 (increase of $1,000) for Married Filing Jointly.

Child Tax Credit

The maximum credit per qualifying child is $2,000. The definition of a qualifying child has not changed. The refundable amount of the credit is limited to $1,400 per qualifying child.

Earned Income Credit (EIC)

For 2019, the maximum credit increased to:

$6,557 with three or more children

$5,828 with two children

$3,526 with one child

$529 with no children

To be eligible for a full or partial credit, the taxpayer must have earned income of at least $1 but less than:

$50,162 ($55,952 if Married Filing Jointly) with three or more qualifying children

$46,703 ($52,493 if Married Filing Jointly) with two qualifying children

$41,094 ($46,884 if Married Filing Jointly) with one qualifying child

$15,570 ($21,370 if Married Filing Jointly) with no qualifying child

Investment Income

Taxpayers whose investment income is more than $3,600 cannot claim the EIC.

Education Benefits

American opportunity credit for 2019 is gradually reduced (phased out) if taxpayers' MAGI is between $80,000 and $90,000 ($160,000 and $180,000 if Married Filing Jointly). Taxpayers cannot claim a credit if their MAGI is $90,000 or more ($180,000 or more if Married Filing Jointly).

Lifetime learning credit for 2019 is gradually reduced (phased out) if taxpayers' MAGI is between $58,000 and $68,000 ($116,000 and $136,000 if Married Filing Jointly). Taxpayers cannot claim a credit if their MAGI is $68,000 or more ($136,000 or more if Married Filing Jointly).

Student loan interest deduction begins to phase out for taxpayers with MAGI in excess of $70,000 ($140,000 for joint returns) and is completely phased out for taxpayers with MAGI of $85,000 or more ($170,000 or more for joint returns).

Affordable Care Act

Filing thresholds and federal poverty line tables have been adjusted for inflation.

For 2019, the shared responsibility payment (SRP) is zero. Taxpayers who do not have health insurance coverage during 2019 or later do not require an exemption to avoid the SRP.

Details about these and other updates can be found in the Affordable Care Act lesson and in Publication 4012 Tab H, Other Taxes, Payments, and ACA.

IRAs and Other Retirement Plans

Modified Adjusted Gross Income (AGI) Limit (Advanced certification)

For 2019, the maximum IRA deduction increases to $6,000 ($7,000 if age 50 or older). If a taxpayer is covered by a retirement plan at work, the deduction for contributions to a traditional IRA is reduced (phased out) if the modified AGI is:

More than $103,000 but less than $123,000 for Married Filing Jointly taxpayers or Qualifying Widow(er) if both spouses are covered by a retirement plan

More than $64,000 but less than $74,000 for a Single or Head of Household or

Less than $10,000 for Married Filing Separately

For an IRA contributor who is not covered by a workplace retirement plan and is married to someone who is covered, the deduction is phased out if the couple's income is between $193,000 and $203,000.

Kiddie Tax

For 2019, Form 8615 must be filed for certain children who had more than $2,200 of unearned income.